How to Dispute a Total Loss Settlement Offer

If your insurance company’s total loss settlement offer seems too low, you do not have to assume their number is final.

You may be able to dispute the valuation by identifying errors, weak comparable vehicles, missing options, or unfair condition adjustments.

The key is to challenge the offer with specific evidence, not general frustration.

Why Total Loss Settlement Offers Get Disputed

A total loss offer is usually based on a valuation report that estimates your vehicle’s pre-loss value. If that report is inaccurate, the settlement can be inaccurate too.

People often dispute a total loss valuation when:

- The comparable vehicles do not match the year, trim, mileage, or condition of their car

- The report missed important options or packages

- The insurer used vehicles from an irrelevant market

- The condition adjustments seem unfair

- The offer does not reflect what it would realistically cost to replace the vehicle

In other words, the problem is often not that the insurer used a valuation process. The problem is that the process may have used the wrong inputs.

Signs the Offer May Be Too Low

Not every total loss settlement is wrong, but some warning signs show up repeatedly.

You may have reason to challenge the offer if:

- The amount is much lower than expected based on your vehicle and market

- The insurer’s report includes errors in trim, mileage, options, or condition

- The comparable vehicles are poor matches

- The valuation ignores meaningful upgrades or equipment

- The report relies on questionable adjustments

- The settlement would not reasonably allow you to replace the vehicle with a similar one

A low-ball total loss offer is often tied to details that can be documented and disputed.

How to Dispute a Total Loss Valuation

A stronger dispute starts with a clear review of the insurer’s valuation report.

1

Read the valuation report carefully

Do not focus only on the final number. Review the details used to get there, including:

- Year, make, model, and trim

- Mileage

- Options and package

- Vehicle condition

- Comparable vehicles

- Adjustment amounts

- Geographic market area

Small errors can produce a materially lower value.

2

Look for weak comparable vehicles

Comparable vehicles are one of the most important parts of the report. If the comps are not truly comparable, the conclusion may be flawed.

Watch for comps that:

- Have different trims or major equipment differences

- Have much higher mileage

- Are in a different market

- Are not actually similar in condition

- Do not reflect realistic replacement options

3

Gather supporting documentation

Evidence matters more than opinions. Depending on your situation, useful documentation may include:

- The insurer’s valuation report

- Photos of your vehicle before the loss

- Maintenance and condition records

- Documentation of options, upgrades, or packages

- Purchase records or window stickers, if available

- Independent market data

The goal is to show where the insurer’s valuation may have missed the mark.

4

Respond with specific challenges

A weak dispute says the offer “feels too low.” A stronger dispute identifies what appears incorrect and why.

Examples of focused dispute points include:

- The trim level appears to be wrong

- The mileage is inaccurate

- Key options were not included

- The comparable vehicles are not sufficiently similar

- The condition adjustments appear unsupported

- The market selection does not reflect relevant replacement vehicles

5

Consider an independent total loss appraisal

An independent appraisal can help when you need a documented, evidence-based review of the insurer’s valuation.

This can be especially useful when:

- The report is complex

- The insurer is not responding to informal pushback

- You want a professional review before accepting the offer

- You need support for a more formal dispute

Case Study: How DVAC Secured an Extra $9K for a Totaled Truck

Slip sliding away. A young woman was referred to DVAC by her auto body shop. An at fault insured driver hydroplaned on I-95, in a panic the other driver slammed the brakes halting to a stop from 70Mph. As a result the young lady swiped the other vehicle and then lost control, hitting a telephone pole. The 2021 Nissan Titan with only 8224 miles on the clock was totaled. The at fault insurance company offered an insulting $51,332.83 and wouldn’t

Case Study: How DVAC Secured an Extra $9K for a Totaled Truck

Slip sliding away. A young woman was referred to DVAC by her auto body shop. An at fault insured driver hydroplaned on I-95, in a panic the other driver slammed the brakes halting to a stop from 70Mph. As a

Where an Independent Appraisal Fits

A total loss appraisal is not just another opinion. It is an independent review of the valuation logic, comparable vehicles, condition analysis, and market support behind the insurer’s offer.

That can help you:

- Identify flaws in the original report

- Understand whether the offer is reasonable

- Build a more credible dispute

- Support negotiations with objective documentation

- Help achieve a more favorable resolution under the appraisal clause if the current offer is determined to be too low

If the issue is real, independent evidence gives you a better chance of challenging the settlement effectively.

Mistakes to Avoid When Disputing a Total Loss Offer

Many people weaken their position by approaching the dispute the wrong way.

Avoid these common mistakes:

- Accepting the first offer before reviewing the report

- Relying only on random online listings

- Arguing emotionally instead of factually

- Missing errors in trim, options, mileage, or condition

- Waiting too long to gather evidence

- Assuming the insurer’s valuation system must be correct

The dispute process is usually more effective when it is precise, documented, and focused on valuation details.

What to Do Next

If you believe the settlement is too low, start by reviewing the insurer’s valuation report closely. Look for factual errors, weak comps, missing equipment, and unsupported adjustments. If the problems are not easy to resolve on your own, an independent appraisal may help clarify whether the valuation should be challenged.

Real Reviews, Real Results

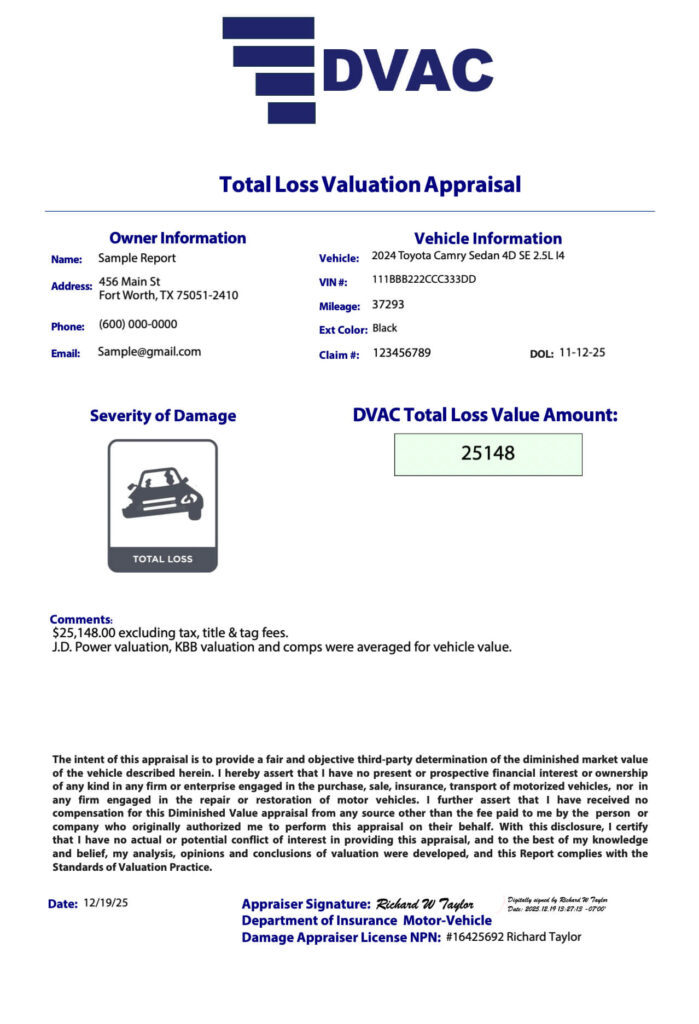

Total Loss Appraisal Report:

Wondering what’s in a DVAC appraisal? Take a look at this recent appraisal we completed for a client.

Frequently Asked Questions

Can I dispute a total loss settlement offer?

Yes. If you believe the valuation is inaccurate, you can challenge it with evidence and documentation. The strength of the dispute usually depends on the quality of the facts behind it.

What is the best way to challenge a low-ball total loss offer?

The strongest approach is to identify specific issues in the valuation report, support them with documentation, and present a clear, evidence-based dispute.

Should I accept the first total loss offer?

Not until you understand how the number was calculated and whether the report appears accurate.

What if I do not understand the insurer’s valuation report?

That is a common problem. An independent total loss appraisal can help review the report and identify whether the valuation appears supportable.

Is disputing a total loss settlement the same as getting legal advice?

No. Disputing valuation is not the same as receiving legal advice. If your claim involves legal issues, deadlines, or policy interpretation, you may also want to speak with an attorney.

Get Help Reviewing Your Total Loss Offer

If your settlement offer looks low, MYDVAC can help review the valuation and identify whether it should be challenged. A professional total loss appraisal can give you a clearer picture of what your vehicle was worth and whether the insurer’s number holds up.

Get a total loss appraisal review.

Start The Total Loss Appraisal Process

If your insurer’s offer does not look right, do not rely on guesswork. DVAC can review the valuation, identify problems, and provide an independent total loss appraisal to help you challenge a low settlement offer.

No obligation required.

A+ Rating on BBB | Servicing Clients Nationwide