Total Loss Appraisal

How to Challenge a Low Insurance Offer.

Don’t let an automated software determine your car’s worth. Get a human-led market analysis.

When an insurance company declares your vehicle a total loss, the settlement offer should reflect what your car was actually worth before the accident. If the number feels low, a total loss appraisal can help you challenge that valuation with independent market-based evidence.

MYDVAC provides independent total loss appraisals designed to identify undervaluation, support a stronger dispute, and help you pursue a fairer settlement.

What Is a Total Loss Appraisal?

A total loss appraisal is an independent evaluation of your vehicle’s value before it was declared a total loss. Its purpose is to determine whether the insurance company’s offer is supported by accurate data, relevant comparable vehicles, and a fair assessment of your vehicle’s condition, options, mileage, and market.

This matters because the insurer’s valuation is often the foundation of the settlement offer. If that valuation is flawed, the settlement may be too low.

When Should You Get a Total Loss Appraisal?

A total loss vehicle appraisal may make sense if:

- The insurance company’s offer seems lower than expected

- The comparable vehicles in the report do not look like yours

- Important features, upgrades, or package options were overlooked

- The vehicle condition was rated unfairly

- The valuation report contains errors in mileage, trim, or equipment

- You want independent evidence before accepting the settlement

In many cases, policyholders know something is off but do not have the documentation or valuation support needed to push back effectively. That is where an independent appraisal can help.

Why Total Loss Settlement Offers Can Be Too Low

Insurance companies usually rely on valuation systems, third-party reports, and internal processes to determine what they are willing to pay. Those systems are not always wrong, but they are not always complete or accurate either.

A settlement offer can come in low when:

- The comparable sales are weak or poorly matched

- The report uses vehicles from the wrong market area

- Equipment or trim differences are missed

- Vehicle condition is adjusted unfairly

- Mileage adjustments are inaccurate

- Dealer asking prices and real market behavior are not interpreted correctly

How a Total Loss Appraisal Helps You Dispute a Low Offer:

If the insurer’s number is based on incomplete or flawed valuation logic, a total loss appraisal gives you independent documentation to support your position.

That can help you:

1. Understand whether the offer is reasonable

2. Identify specific weaknesses in the insurer’s report

3. Present a stronger challenge with evidence instead of opinion

4. Support negotiations for a higher settlement

5. Move forward with more confidence and clarity

For many vehicle owners, the issue is not just frustration. It is whether the settlement reflects the real value of the vehicle they lost.

How MYDVAC Evaluates Vehicle Value:

MYDVAC takes an independent, evidence-based approach to total loss valuation. The goal is not to inflate numbers. The goal is to determine a credible, supportable value based on the available market data and vehicle facts.

Our total loss appraisal process may include:

1. Reviewing the insurer’s valuation report

2. Examining the comparable vehicles used in the calculation

3. Looking for errors in trim, options, mileage, or condition

4. Identifying whether the comps are truly comparable

5. Evaluating the local or relevant vehicle market

6. Building a documented, supportable appraisal that can be used in a dispute

This gives you a clearer basis for deciding whether to accept the offer or challenge it.

Case Study: How DVAC Secured an Extra $9K for a Totaled Truck

Slip sliding away. A young woman was referred to DVAC by her auto body shop. An at fault insured driver hydroplaned on I-95, in a panic the other driver slammed the brakes halting to a stop from 70Mph. As a result the young lady swiped the other vehicle and then lost control, hitting a telephone pole. The 2021 Nissan Titan with only 8224 miles on the clock was totaled. The at fault insurance company offered an insulting $51,332.83 and wouldn’t

Case Study: How DVAC Secured an Extra $9K for a Totaled Truck

Slip sliding away. A young woman was referred to DVAC by her auto body shop. An at fault insured driver hydroplaned on I-95, in a panic the other driver slammed the brakes halting to a stop from 70Mph. As a

Common Mistakes After a Total Loss Offer:

After receiving a total loss insurance settlement offer, people often make avoidable mistakes that weaken their position.

A settlement offer can come in low when:

- Accepting the first offer too quickly

- Focusing only on asking prices they find online

- Ignoring errors in the insurer’s report

- Assuming the valuation system must be correct

- Waiting too long to gather supporting evidence

- Arguing generally instead of challenging specific valuation issue

A stronger dispute usually starts with objective documentation and a clear explanation of what is wrong with the valuation.

Why Work With MYDVAC

MYDVAC is focused on helping consumers challenge questionable insurance valuations with objective support. Clients come to us because they want:

An independent review of the insurer’s valuation

We use real market data from sources like Carfax to provide precise and defensible valuations.

A report grounded in real market data

Our methodology is accepted by insurance companies, ensuring your claim stands up to scrutiny.

Clear documentation they can use in a dispute

we provide honest valuations that reflect your vehicle’s true worth, ensuring you receive the compensation you deserve.

Experienced guidance through the process

We don’t just send a report—we handle the negotiations under the appraisal clause with the insurance company's hired third party.

A report grounded in real market data

Our clients successfully recover diminished value in nearly every case.

Real Reviews, Real Results

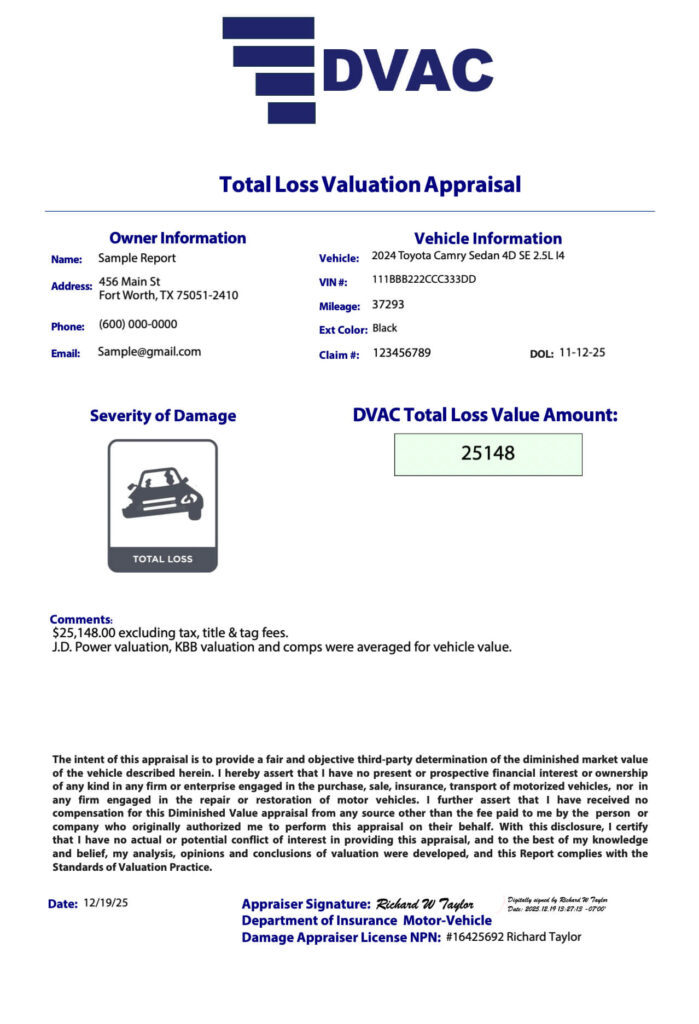

Total Loss Appraisal Report:

Wondering what’s in a DVAC appraisal? Take a look at this recent appraisal we completed for a client.

Frequently Asked Questions

What is the difference between a total loss appraisal and the insurer’s valuation?

The insurer’s valuation is produced as part of the claims process to support its settlement offer. A total loss appraisal is an independent review intended to determine whether that valuation is accurate and fair.

Can a total loss appraisal help increase my settlement?

Yes, if we determine the value is too low, we can get more money through the appraisal clause process. It can help support a dispute when the original valuation appears too low. Results vary by claim, policy, evidence, and insurer response, but a well-supported appraisal gives you a stronger basis for challenging the offer.

When should I get a total loss appraisal?

Before accepting the settlement, especially if you believe the valuation is too low or the report contains errors.

What if the insurer used a CCC report?

A CCC-based valuation can still be challenged if the underlying data, comp selection, adjustments, or condition ratings appear flawed. An independent review can help identify those issues.

Is this the same as legal advice?

No. A total loss appraisal is a valuation service, not legal advice. Every policyholder has a right to a third-party appraisal. If your situation involves policy interpretation, legal deadlines, or state-specific rights, you may also want to consult an attorney.

Start The Total Loss Appraisal Process

If your insurer’s offer does not look right, do not rely on guesswork. DVAC can review the valuation, identify problems, and provide an independent total loss appraisal to help you challenge a low settlement offer.

No obligation required.

A+ Rating on BBB | Servicing Clients Nationwide