Actual Cash Value vs Fair Market Value for a Totaled Car

When your car is declared a total loss, the insurance settlement is often based on actual cash value, or ACV. But many vehicle owners compare that number to what they believe the car was worth in the real market. That is where confusion starts.

Understanding actual cash value vs fair market value for a totaled car can help you evaluate whether the insurer’s offer makes sense or whether the valuation may be too low.

What Is Actual Cash Value?

Actual cash value is the amount an insurer says your vehicle was worth immediately before the loss, after accounting for factors like age, mileage, condition, depreciation, and market data.

In a total loss claim, ACV is often the number used to support the settlement offer.

Insurance companies typically calculate actual cash value using valuation reports, comparable vehicles, condition adjustments, and proprietary systems. The exact method can vary, but the result is meant to represent the vehicle’s pre-loss value, not what you originally paid for it and not necessarily what it would cost to buy the same car today under ideal conditions.

What Is Fair Market Value?

Fair market value generally refers to the price a willing buyer would pay and a willing seller would accept for the vehicle in an open market.

In practical terms, fair market value is often how consumers think about replacement value. They look at what similar vehicles are listed or selling for and ask whether the insurer’s number reflects the real market.

That does not mean every online listing proves fair market value. But it does mean there can be a meaningful gap between a valuation report and what a comparable vehicle appears to be worth in the real world.

This matters because the insurer’s valuation is often the foundation of the settlement offer. If that valuation is flawed, the settlement may be too low.

Actual Cash Value vs Fair Market Value: What Is the Difference?

The difference is not always absolute. In theory, ACV is supposed to reflect a fair market-based value. In practice, the insurer’s ACV calculation may be lower than what the owner sees as fair market value because of the way the valuation was built.

The gap often comes from:

- Questionable comparable vehicles

- Aggressive condition adjustments

- Missing options or trim details

- Mileage errors

- Weak market selection

- Valuation methods that do not reflect realistic replacement value

So the issue is often not that ACV and fair market value are unrelated. The issue is whether the insurer’s ACV actually reflects a fair and supportable market value.

Why This Difference Matters in a Total Loss Claim

If the insurer’s actual cash value is too low, your total loss settlement may also be too low.

That matters because the settlement is supposed to compensate you for the value of the vehicle you lost. If the valuation is built on flawed inputs, the offer may fall short of what the car was actually worth before the accident.

This is why many disputes focus less on abstract definitions and more on whether the valuation report itself is accurate.

How Undervaluation Happens

A totaled car can be undervalued when the insurer’s report relies on weak or inaccurate information.

Common examples include:

- The trim level is wrong

- Key options or packages are missing

- The comparable vehicles are poor matches

- The report uses vehicles from the wrong market

- The condition rating is overly negative

- Mileage is entered incorrectly

- Adjustments reduce the value without strong support

Even if the report looks technical, the output is only as good as the data and assumptions behind it.

When to Question the Insurance Company’s Valuation

You may have reason to look more closely if:

- The offer feels much lower than expected

- The insurer’s report contains factual errors

- The comparable vehicles are not truly similar

- The number would not allow you to replace the vehicle with a comparable one

- The settlement seems disconnected from real-world market conditions

A low number alone is not enough to prove undervaluation. But a low number plus valuation problems is a reason to investigate further.

When to Get a Total Loss Appraisal

If you believe the insurer’s actual cash value does not reflect a fair market-based valuation, an independent appraisal can help.

A total loss appraisal may make sense when:

- You want a professional review of the insurer’s valuation

- You suspect the report contains errors

- You need evidence to support a dispute

- You are deciding whether to accept or challenge the settlement

An independent review can help determine whether the ACV appears reasonable or whether the valuation may be too low.

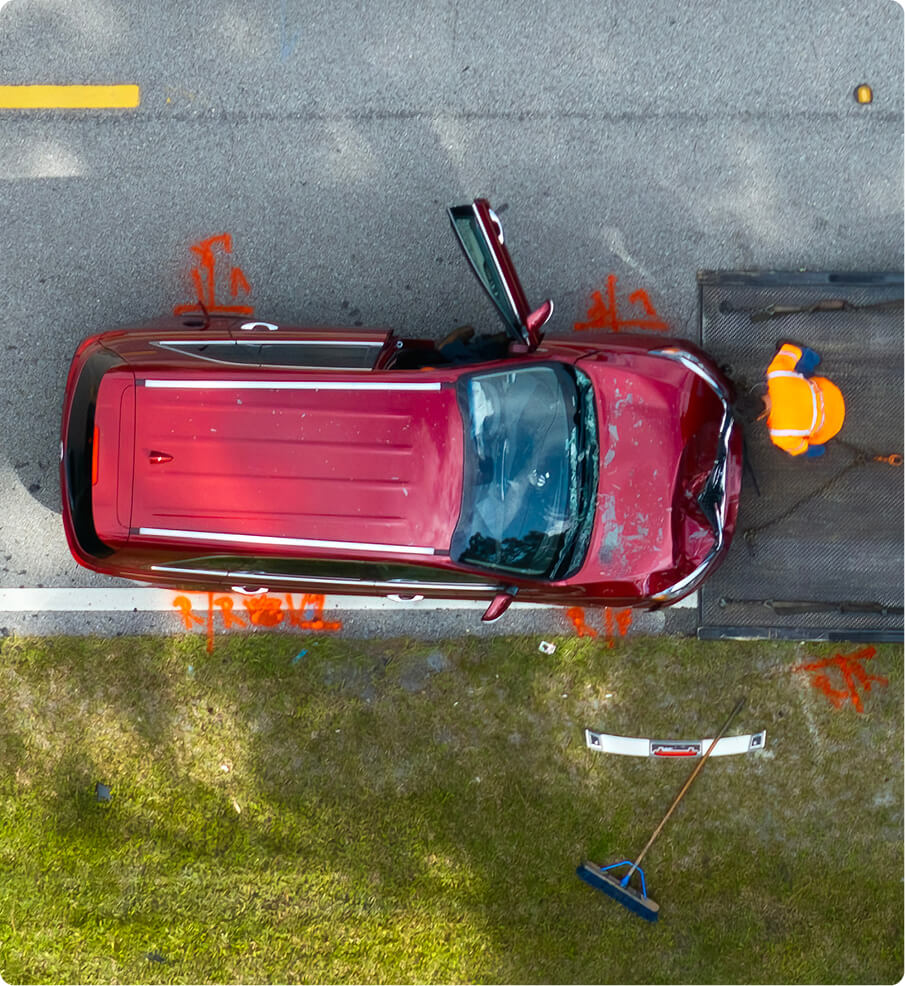

Case Study: How DVAC Secured an Extra $9K for a Totaled Truck

Slip sliding away. A young woman was referred to DVAC by her auto body shop. An at fault insured driver hydroplaned on I-95, in a panic the other driver slammed the brakes halting to a stop from 70Mph. As a result the young lady swiped the other vehicle and then lost control, hitting a telephone pole. The 2021 Nissan Titan with only 8224 miles on the clock was totaled. The at fault insurance company offered an insulting $51,332.83 and wouldn’t

Case Study: How DVAC Secured an Extra $9K for a Totaled Truck

Slip sliding away. A young woman was referred to DVAC by her auto body shop. An at fault insured driver hydroplaned on I-95, in a panic the other driver slammed the brakes halting to a stop from 70Mph. As a

Common Misunderstandings

- “Actual cash value is whatever the insurer says it is”

Not necessarily. The insurer provides its valuation, but that does not make it automatically accurate or beyond challenge. - “Fair market value just means the highest asking price I can find”

No. A fair market view should be based on credible comparable vehicles and realistic market evidence, not cherry-picked listings. - “If the report looks official, it must be correct”

Not always. Formal reports can still contain weak comps, missing data, or unsupported adjustments.

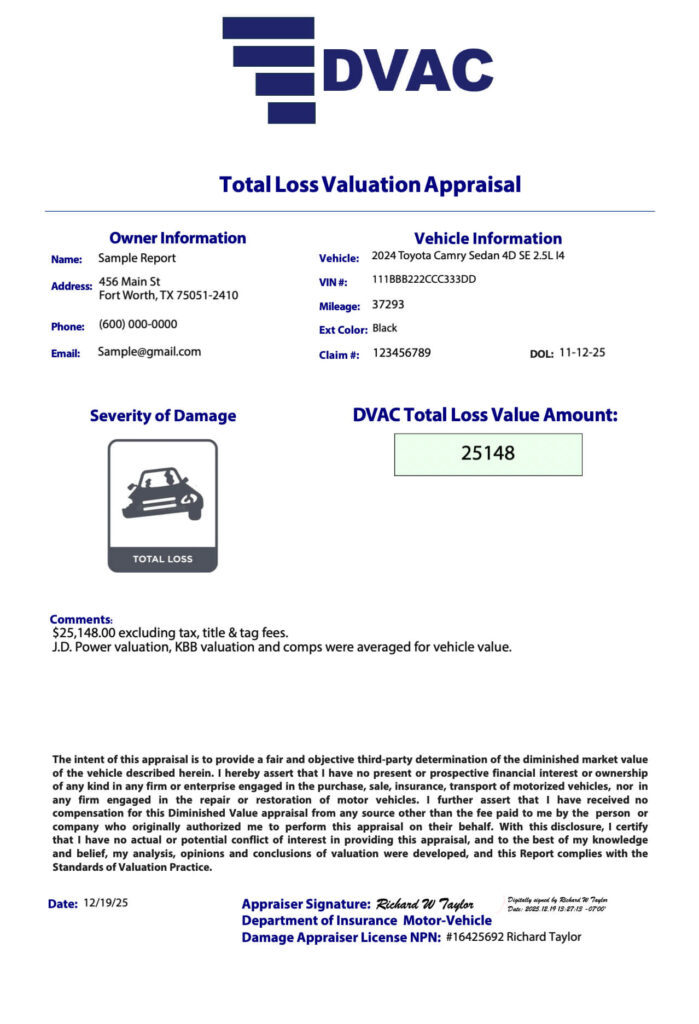

Real Reviews, Real Results

Total Loss Appraisal Report:

Wondering what’s in a DVAC appraisal? Take a look at this recent appraisal we completed for a client.

Frequently Asked Questions

Is actual cash value the same as fair market value?

Not always in practice. ACV is supposed to reflect a market-based pre-loss value, but the insurer’s calculation may differ from what the real market suggests if the valuation inputs are flawed.

Why is my actual cash value lower than expected?

Possible reasons include depreciation, condition adjustments, weak comparable vehicles, missing options, mileage errors, or other valuation issues.

Can I dispute the ACV on a totaled car?

Yes. If the insurer’s valuation appears inaccurate, you may be able to challenge it with documentation and independent evidence.

What matters more in a total loss claim, ACV or fair market value?

The settlement is usually based on ACV, but the real issue is whether that ACV is a fair and supportable reflection of the vehicle’s market value.

Should I get an appraisal if I think the ACV is too low?

It may be worth considering if the report appears flawed or the settlement offer seems materially below a credible market value.

Find Out Whether Your Valuation Is Too Low

If the insurer’s actual cash value does not seem to reflect what your totaled car was really worth, MYDVAC can help review the valuation and identify whether there are grounds to challenge it.

A total loss appraisal can provide independent support when the settlement offer does not hold up.

Request a valuation review today.

A+ Rating on BBB | Servicing Clients Nationwide