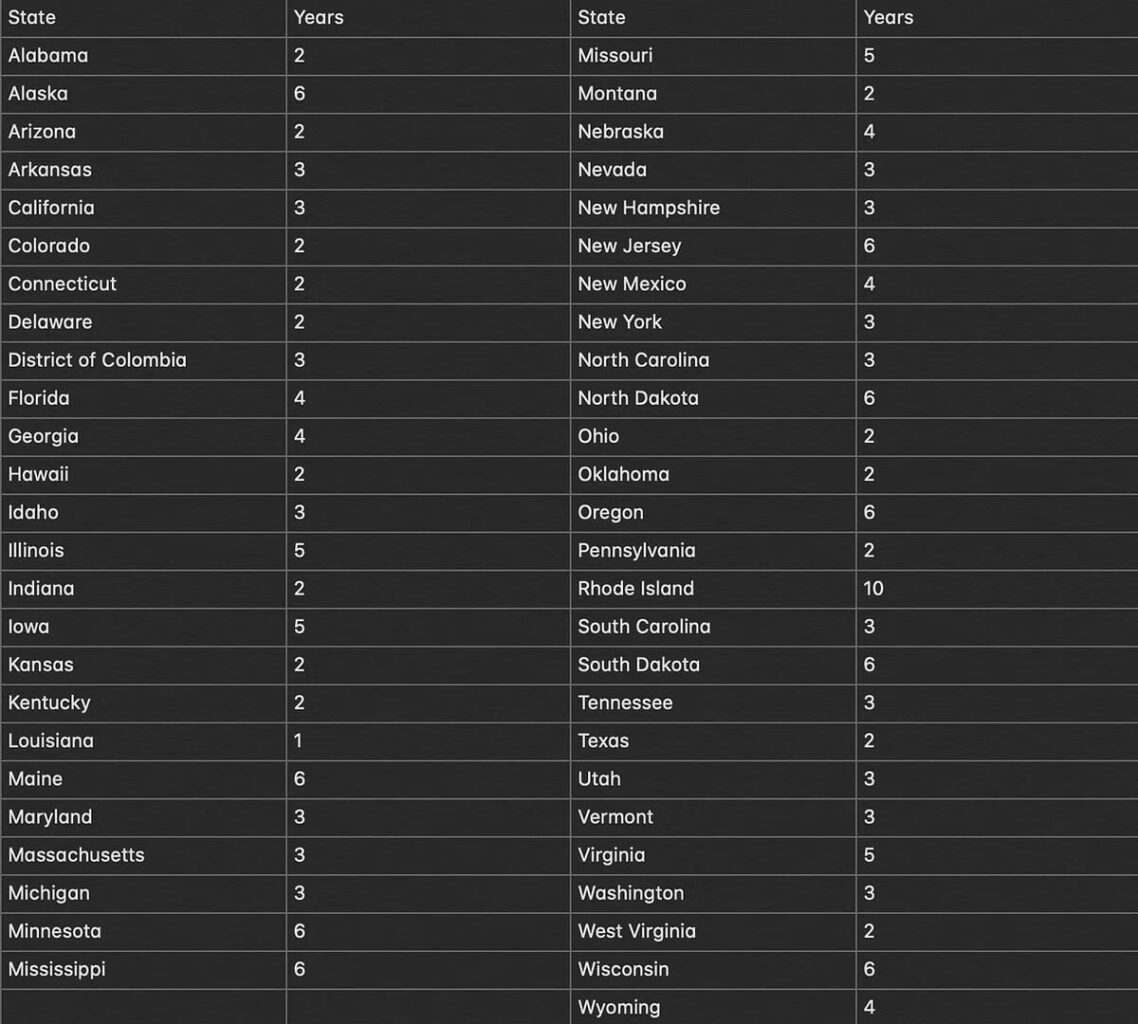

Diminished value is recoverable in third-party cases and through your own uninsured motorist coverage. Minimum liability coverage is required and the statute of limitations to file a claim is 2 years from the date of the accident. § 34-51-2-19.

Wiese-GMC, Inc. v. Wells, 626 N.E.2d 595 (Ind. Ct. App. 1993)

The fundamental measure of damages in a situation where an item of personal property is damaged, but not destroyed, is the reduction in fair market value caused by the negligence of the tortfeasor. This reduction in fair market value may be proved in any of three ways, depending on the circumstances.

First, it may be proved by evidence of the fair market value before and the fair market value after the causative event.

Second, it may be proved by evidence of the cost of repair where repair will restore the personal property to its fair market value before the causative event.

Third, the reduction in fair market value may be proved by a combination of evidence of the cost of repair and evidence of the fair market value before the causative event and the fair market value after repair, where repair will not restore the item of personal property to its fair market value before the causative event.

Indiana Code Title 27. Insurance § 27-7-5-2

(1) in limits for bodily injury or death and for injury to or destruction of property not less than those set forth in IC 9-25-4-5 under policy provisions approved by the commissioner of insurance, for the protection of persons insured under the policy who are legally entitled to recover damages from owners or operators of uninsured or underinsured motor vehicles because of bodily injury, sickness or disease, including death, and for the protection of persons insured under the policy who are legally entitled to recover damages from owners or operators of uninsured motor vehicles for injury to or destruction of property resulting therefrom; or UMPD coverage is for the insured who is “legally entitled to recover damages from owners or operators of uninsured motor vehicles for injury to or destruction of property resulting therefrom.”

Ind. Code §27-7-5-2(a)(1).

As a condition precedent to UMPD coverage, the insured must establish that there is no insurance policy covering the tortfeasor or motor vehicle.

See Michael v. Wolfe, 737 N.E.2d 820, 822 (Ind. Ct. App. 2000).

Dunn v. Meridian Mut. Ins. Co., 836 N.E.2d 249 (Ind. 2005)

Court ruled that diminished value is covered by your UIM policy when the at-fault driver is uninsured.